Magazine

Do You Thrive To Learn More About How To Achieve Greater Business Success?

Sign up to our magazine designed specifically for Australian business leaders.

Our Perth-based team of tax accountants can assist you with the setup of an SMSF including Bare Trust for the purposes of a Limited Recourse Borrowing Arrangement associated with real estate.

Thereafter, we can assist with ongoing annual compliance obligations such as the annual tax return.

Please note, our involvement is strictly limited to accounting solutions. We do not provide financial/investment advice.

The Superannuation Laws require the Trustee of a SMSF to use a Bare Trust to hold the legal title of any single acquirable asset when under a limited recourse borrowing arrangement (LRBA). E.g. Real estate that has been purchased with finance. Ordinarily, the Trustee of the Bare Trust must be a company to satisfy bank requirements.

Buying an investment property within a SMSF using an LRBA involves setting up a company and preparing LRBA documentation, which typically includes establishment of a Bare Trust Deed, SMSF Trustee Minutes, Loan Agreement, Security Agreement and other legal documents.

Typically, before shopping for a property you will be required to work with your financial advisor and potential lenders so you can be granted finance pre-approval.

If you need a SMSF loan, before establishing a Bare Trust you will need the property’s details. While it may seem like a step out of sequence, it’s important to note that supplying us with the property details is a preliminary requirement for establishing the Bare Trust.

Once you have found a property and established a Bare Trust it’s then possible to formally proceed with applying for the loan. This process may take longer than a normal home loan because of the documentation required. In a hot property market where 21 or 30-day settlements are common, this means quick action is probably necessary if you want to secure the property you’re interested in.

Price – Bare Trust & LRBA

Set out below is the pricing for the establishment of a Bare Trust and LRBA:

This includes legal and regulatory (ASIC) fees. (The setup of a SMSF is separate.)

Please note that this price only applies if you are obtaining finance from a bank or a financier that is a 3rd party dealing with the SMSF on an arm’s length basis. If you are planning to obtain finance from a related entity (i.e. non-arm’s length loan), then the price to prepare the LRBA documentation will need to be revised (estimated total cost will increase to $6,600 including GST). This is because further documentation will need to be tailored because a non-arm’s length loan exists.

video key points

Presented by: Sanjay Nair

video transcript

When considering property investment within a Self-Managed Superannuation Fund, there are several key factors to keep in mind.

The first thing a prudent trustee will consider is the suitability of owning real estate in the SMSF. You need to evaluate whether the SMSF has enough funds to justify the annual compliance costs, which typically start around $3,000 and increase from there, especially when borrowing is involved. A balance of $300,000 is often considered the minimum, but this is just one factor.

The Australian corporate regulator, ASIC, has developed case studies which we link to on our website. Generally, it’s advisable to seek financial advice from a licensed advisor to help assess suitability.

Assuming you determine it is suitable to purchase real estate in a SMSF, you’ll need to ensure the rules of the fund permits this. The Super Laws broadly allow you to use debt to acquire real estate, but the conditions are strict. You will need to use a “Limited Recourse Borrowing Arrangement”, and the property must be registered in the name of a custodian using a Bare Trust.

The money can be borrowed from a third party, such as a bank, or from a related party. Regardless, the terms must always be at ordinary market rates and conditions.

If investing in property through your SMSF is something you’d like to pursue, we can help with accounting solutions.

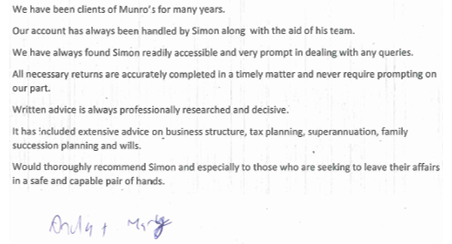

Professional, insightful and always supporting. Christine and Munro’s has helped me through all avenue’s and queries regarding investment, tax return, property, super and general finance. Really appreciative of their work and highly recommend!

Excellent accounting service with a deep understanding of tax implications for SMSFs.

I was very impressed with Munro’s accounting service. Before I engaged with Munro’s, I met with accountants across Australia, but I decided to go with Munro’s because of their breadth and understanding of taxation.

Brian from Munro’s was able to quickly and efficiently complete my 2023 tax returns, and also provided additional advice and expertise on how I could better structure my affairs.

Originally, I briefed Munro’s to wind back my SMSF due to the administrative burden of managing it. However, Munro’s was able to clearly understand my affairs and prepare the tax documentation in a way that reduced the administrative burden. I was so impressed with their service that I decided to continue with the SMSF after all.

I highly recommend Munro’s to anyone looking for an accounting service with a deep understanding of taxation and SMSFs.

Do You Thrive To Learn More About How To Achieve Greater Business Success?

Sign up to our magazine designed specifically for Australian business leaders.